Foreign investment in UK property is a hot topic at the moment. Some people view it as an essential part of the economy, propping up a housing market that would otherwise start to wobble.

Not everyone feels that way, though. You’ll hear people frequently say that foreign investment is a leading cause in the unaffordability crisis, and creates difficulty for first-time buyers to get onto the ladder.

To find out where the truth lies, it’s useful to step back, and take a wider perspective on foreign investment in UK property.

Unlike decades gone by, foreign buyers aren’t focusing all their attention on London anymore. While the capital city remains the area with the most investment, foreign money is also going towards family homes, blocks of flats, student lets, and more.

Some are genuine long-term investors, while others are lifestyle buyers. There’s also a growing pattern of foreign investors buying a ‘Plan B’ passport route for their children, so they can study in the UK further down the line.

The UK remains an attractive place to invest in property, regardless of where you’re from. So, what’s really going on? How much foreign investment is there? And where is it coming from?

Let’s get into it.

The big numbers: what foreign investment really looks like

Foreign investment in UK property is a growing part of the market.

According to Search Acumen data, the number of property titles owned by overseas companies in England and Wales has risen from 47,787 in 2015 to 91,791 in 2025. That’s a 92% increase in just ten years.

The value of that property is even more eye-opening. Collectively, those 91,791 overseas-owned properties are estimated to be worth more than £125 billion. Back in 2015, overseas-held property was valued at £15.9 billion.

So, while the number of properties owned by foreign investors has doubled, the value of that housing stock has multiplied by 10.

Search Acumen also states that the value of UK property assets held by overseas companies is now at an all-time high, jumping 44% in three years, equal to £38.5 billion.

And yet, there’s an interesting twist. The data also suggests the total number of overseas company titles actually fell slightly, with 3,834 fewer titles in 2025 than 2022.

So fewer properties, but far more value. It seems that the money is flowing into high-end areas around the UK, and concentrating on premium assets.

How much property is really owned by foreign investors?

You might come across the argument that foreign investment is taking over the UK market. Well, while there’s no doubt that it’s growing quickly, that statement isn’t strictly true.

Some estimates suggest around 250,000 properties in the UK are owned by foreign individuals. This is out of roughly 27 million homes, which puts it at less than 1%.

So no, Britain hasn’t been ‘sold off’. Although, that’s not to say that foreign investment isn’t affecting the market: their ownership of the most desirable parts of the country is far bigger than 1%, which gives birth to the narrative.

How foreign buying actually works

When you think about foreign buying, you might picture a wealthy investor flying in on a private jet, walking around several mansions, and writing a cheque.

That’s not quite the reality. Buying a UK property needs to be carefully structured for foreigners.

Plenty of overseas buyers buy through UK limited companies or offshore entities. This is mainly done for tax planning, inheritance planning, or privacy.

In August 2022, the UK introduced the Register of Overseas Entities, forcing overseas companies that own UK property to declare their beneficial owners.

It had an impact. Search Acumen data shows Jersey has now overtaken the British Virgin Islands as the most popular jurisdiction for holding UK property wealth through overseas companies, with £57 billion worth of UK assets.

The British Virgin Islands sit second at 21%, Guernsey at 13%, and the Isle of Man at 11%.

That’s not a coincidence. Investors go where the legal frameworks are stable and the structures are familiar.

Meanwhile, getting a UK mortgage as a foreign buyer can be relatively straightforward if you’re from a stable country. If you’re from a country with enormous corruption, ongoing conflicts, fluctuating currency, or a difficult diplomatic situation, mortgage companies might put up roadblocks everywhere you go.

London still has the world’s attention

London property continues to attract foreign money – and, according to CBRE, this isn’t just about the property market. It’s also about the English language, the legal system, global connectivity, and the fact London sits in a business-friendly time zone for both east and west.

It’s also about stability. Britain has its political drama, but investors aren’t worried about tanks rolling through Westminster, or the currency going through huge fluctuations. Compared to many countries, the UK is boring in the best way possible.

CBRE states that over the last three years, London received more cross-regional property investment than any other European city. It ranked number one for each of the last three years.

In the 12 months to Q3 2025, London ranked as the second leading global city for cross-border investment volumes, behind Tokyo and ahead of Paris.

Even more telling is the long-term trend. Since 2008, only four cities have seriously competed for top global investment status: London, Paris, New York and Tokyo. Across 71 quarters from Q1 2008 to Q3 2025, London ranked number one more often than any other city analysed.

Statistics also suggest that London has the highest expected 10-year rate of return among major world cities, even after factoring in risk.

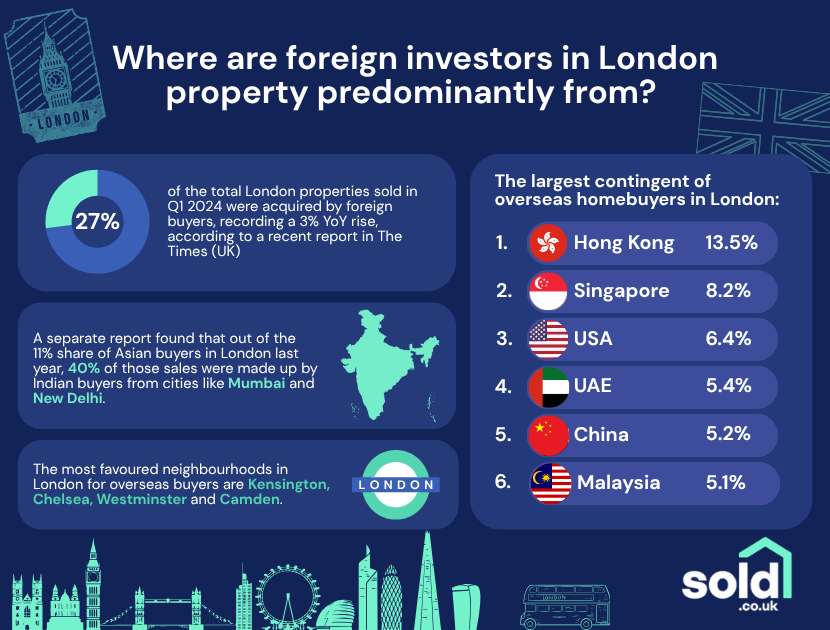

Meanwhile, Benham and Reeves notes that although Kensington, Chelsea, Westminster and Camden remain favourites for overseas buyers, they’re also targeting more affordable Zone 2 areas like Southall, Hayes, West Ham, Woolwich and Wandsworth.

Where is foreign investment coming from?

People and companies from different countries invest in the UK for various reasons, and London is often the centre of that demand.

According to Benham and Reeves research based on FOI data, the largest group of overseas buyers in London in 2024 came from Hong Kong, accounting for over 13.5% of the overseas share.

Next came Singapore at 8.2%. The USA was ranked third at 6.4%, while the UAE was fourth at 5.4%. China is the fifth largest investment source, at 5.2%, while Malaysia followed closely at 5.1%.

Hong Kong investors have poured into the UK in recent years due to political shifts and the desire for stable Western assets. Singapore buyers tend to be high-net-worth investors diversifying internationally.

Americans often buy for lifestyle, education, and long-term capital preservation. Gulf investors buy London as a prestige asset and a financial hedge.

The UK hotspots that foreign investors love

London is the main spot for foreign property investment in the UK, but that money is rapidly expanding into other areas, too. Higher rental yields in northern areas have a lot to do with this.

Irwin Mitchell data on inward investment projects shows London remains dominant, attracting 427 new projects in 2024/25, almost a third of the national total.

There’s been a shift in regional momentum, though, with other areas seeing huge spikes in investment. The West Midlands ranked second with 130 projects, Scotland third with 128, and the North West fourth with 127.

Yorkshire and The Humber followed with 108, while Wales recorded 65 projects, up 23% on the previous year.

So, is foreign investment a good thing?

You won’t be surprised to hear that the answer is both yes, and no.

There’s no doubt that foreign investment fuels development that otherwise wouldn’t happen. This creates jobs, funds regeneration, and keeps the UK competitive.

On the other hand, it also tends to inflate house prices, which could push locals out. This is a particularly difficult pill to swallow when foreign-bought houses sit empty, with no one living in them.

Oxford Academic research examining 1999–2019 data across 332 local authority areas found that a 1% increase in foreign transactions (via overseas companies) raised local house prices by around 0.4%.

The study found that foreign investment pushes up prices across the market, although the effect is stronger at the top end. It also argued that foreign buying doesn’t trigger a ‘meaningful’ increase in construction.

Amongst this, though, arose another ‘red herring’. According to Oxford Academic, foreign investment was actually associated with fewer vacant dwellings, not more. That’s a surprising result for those who insist foreign buyers are leaving entire streets empty.

Property taxes for foreign investors: how it works

Foreign buyers pay a 2% stamp duty surcharge on residential purchases, and an additional 5% surcharge if they’re buying an additional property. Companies can face stamp duty rates up to 17%.

So, at first glance, it seems that overseas buyers get hit harder. The truth is slightly more complicated, though.

Moore Kingston Smith highlights one of the biggest differences between individual landlords and corporate landlords: mortgage interest relief.

Individuals no longer deduct mortgage interest from rental profits. Instead, they receive a basic-rate 20% tax credit under Section 24. Companies don’t face this restriction and still deduct interest as an expense.

For the foreign investors that buy in a company, they capitalise on this advantage. Yet, so does every UK landlord that takes the same approach.

Capital Gains Tax is also stricter now. Non-residents must report gains under non-resident CGT rules, based on a 5th April 2019 rebasing, and must report within 60 days of disposal.

Meanwhile, UK residential property is subject to IHT at 40% above the nil-rate band even if held via an overseas company. Holding through a company doesn’t protect non-UK shareholders.

Hidden headaches faced by foreign investors

It’s untrue that foreign investors ‘have it easy’. On the contrary, they often face challenges that native buyers might not.

Navigating the UK’s complex legal system is not a walk in the park. Some of the main areas for confusion include leasehold vs freehold, landlord obligations, and evolving tenant protections. This has been heightened by the recent Renters’ Rights Act bill.

Another major challenge is currency risk. Exchange rates can wipe out returns, so when the pound strengthens, it reduces profits on exit. This isn’t a consideration for native buyers.

Understanding local market dynamics can be a real challenge, and foreign property buyers tend to lean heavily on local experts to combat this. London’s property market is hugely different from Liverpool, or Manchester, or Yeovil, and so on.

Foreign investors also face higher deposit requirements, higher rates, and tougher documentation rules.

So yes, overseas investors often have more money. But they also deal with more complexity and more restrictions than a domestic buyer.

Can global and local house buyers co-exist?

Let’s look at the future of UK property investment.

Foreign investment is not going away. If anything, it will become more important as global wealth expands and digital access makes buying property abroad easier than ever.

The real issue is not whether foreign investors should exist, but whether the legislation surrounding them needs to be strengthened.

Savills research highlights that Singapore now charges a staggering 60% stamp duty rate for non-domestic buyers. Meanwhile, Canada went further and introduced a two-year ban on foreign property purchases, with some exceptions.

Ireland and Portugal ended their golden visa programmes because of affordability concerns. And Los Angeles introduced a transfer tax of 4% on properties above $5 million, rising to 5.5% above $10 million.

Britain has taken steps, but they’ve been timid. A 2% stamp duty surcharge isn’t much in the grand scheme of things.

So, in the long-term, foreign investment in UK property is neither the saviour of the housing market, nor the sole cause of Britain’s affordability crisis. It’s something that needs to be managed carefully, and communicated about clearly.

Otherwise, resentment may start to build-up – even if it’s not based in fact.